In 1999, the Arkansas General Assembly passed Act 1005, legislation cutting the Arkansas capital gains tax. Since that time, recent events have dramatically altered the fiscal landscape at both the federal and state levels. In response to an Arkansas Supreme Court mandate, the Arkansas legislature enacted a large sales tax increase in 2004 to fund education. In 2003, the U.S. Congress dramatically cut the federal capital gains tax, and is now on the verge of passing a federal budget that cuts low-income programs and imposes new costs on states. Given recent events, is it now time for Arkansas to reconsider the capital gains tax cut enacted in 1999? Capital gains are profits or income from the sale of assets, such as stocks, bonds, real estate, etc. Income taxes are paid on these profits only when the assets are sold or “realized.” The capital gain (or income to be taxed) is the difference between the original buying price and the price at the time of sale.

Under Act 1005 of 1999, 30 percent of capital gains income is exempt from the Arkansas income tax, with the remaining 70 percent being taxed as regular income. The act also changed the rate of tax. The Arkansas tax rate on the capital gain now ranges from 1 to 7 percent, depending on the taxpayer’s total taxable income. Arkansas taxpayers do not bear the full cost of any state taxes they pay on capital gains income. Approximately 20 percent of any state capital gains tax can be written off on a taxpayer’s federal income tax (in effect shifting the burden to taxpayers in other states).

In 2004, Arkansas enacted a large sales tax increase (nearly $400 million) to fund education reform. The state sales tax rate was increased by 7/8s of one cent, while a number of small business services were added to the state sales tax base. Low- and middle-income families have borne a disproportionate share of the burden of this tax increase. Low- and middle-income families now pay 12 cents of every dollar they earn in state and local taxes, compared to just 6 cents on the dollar for the top 1 percent of Arkansas’ wealthiest taxpayers.

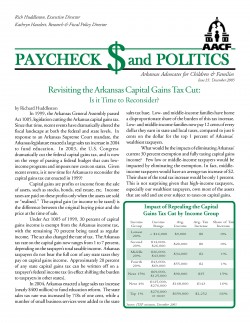

What would be the impacts of eliminating Arkansas’ current 30 percent exemption and fully taxing capital gains income? Few low or middle-income taxpayers would be impacted by eliminating the exemption. In fact, middle-income taxpayers would have an average tax increase of $2. Their share of the total tax increase would be only 1 percent. This is not surprising given that high-income taxpayers, especially our wealthiest taxpayers, own most of the assets that are sold and are ever subject to taxes on capital gains.