In another move by the legislature to give handouts to corporations, HB1045 (now Act 485) will reduce state revenue by tens of millions of dollars annually by reducing the share of corporate profits that are taxable in Arkansas. That’s on top of the tens of millions for mostly out-of-state corporations provided in the large tax cuts in SB549 (Act 532).

This new law will now lead to an increase in “nowhere income” – corporate profits that aren’t taxable in any state, due to a hodgepodge of state and federal tax laws. Instead of reducing state revenue to benefit already profitable corporations, policymakers should be looking at ways to help everyday Arkansans make ends meet.

Throwback Rule

Traditionally Arkansas has used a “three-factor formula,” which uses the share of payroll, property and sales located in-state to calculate corporate income tax liability. This formula reflects the consensus that states that provide public services to a corporation’s property and workers, such as emergency response and schools – not to mention the competitive market and legal rules for a company’s goods to be bought and sold – should be empowered to tax some share of that corporation’s profits.

Since legislation passed in 2019, however, Arkansas has used what is known as a “single sales factor” apportionment, which bases the share of total profit subject to taxes solely on the share of sales in-state.

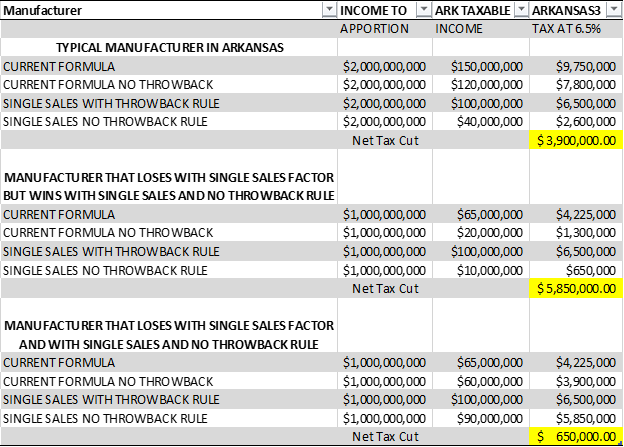

But corporations are not necessarily subject to corporate income taxes in every state in which they sell goods. The throwback rule was intended to ensure that Arkansas’s single sales-factor apportionment formula wouldn’t allow some big corporations to avoid paying a fair share, by having large amounts of “nowhere income” that goes completely untaxed. Moreover, rather than representing an across-the-board tax cut, eliminating the throwback rule is a way to use state tax policy to pick winners and losers. As the Department of Finance and Revenue showed the Legislative Tax Task Force in 2018:

Eliminating the throwback rule reduces revenue in all cases, but some manufacturers are going to win big, seeing their tax liability drop by 90%, while others will see a much more modest reduction of 10%. Most Arkansas-based companies – especially small businesses – likely will not benefit at all from the repeal of the throwback rule, given that big, profitable, and (oftentimes) out-of-state companies are the ones paying the lion’s share of the state’s corporate income tax.

Rather than giving another unnecessary tax cut for corporations already turning a profit, we should have invested in what workers, startups and small businesses, and local Main Streets really need to thrive: early childcare and reliable infrastructure that helps workers get to work, housing assistance that helps everyday Arkansans struggling to make ends meet keep a roof over their heads, first-class schools and affordable college for both young people and returning adults, and other evidence-based investments that create shared prosperity for all Arkansans.