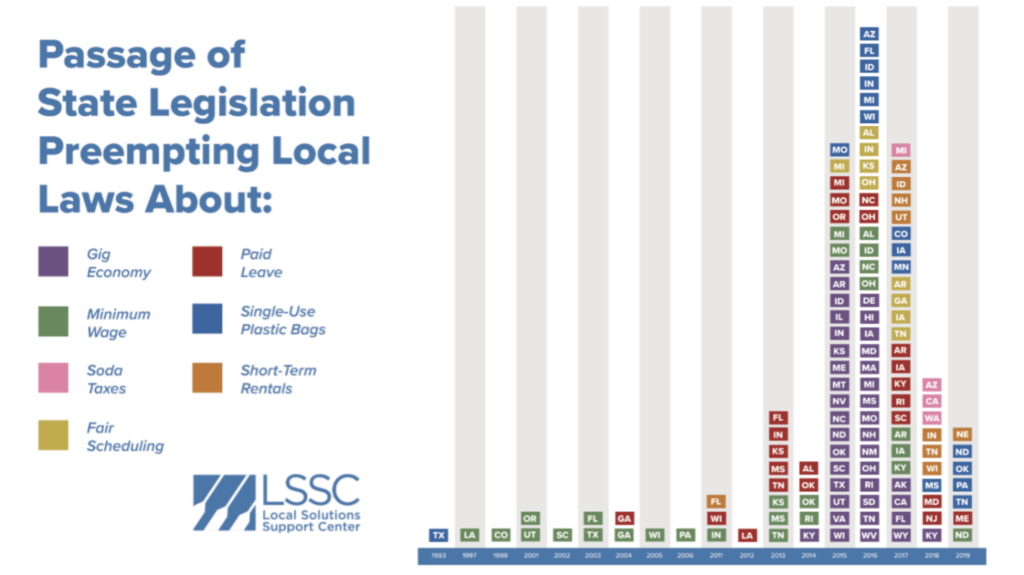

The state legislature in Arkansas – like many others – has increasingly passed laws that limit the ability of cities, counties, and other local governments to set their own agendas based on the needs of their local communities.

One important aspect of local decision-making is the ability of these local governments to raise their own sources of revenue. While federal and state sources of revenue have always been and will always continue to be important sources of revenue for local government, there are both economic and political efficiencies to local governments having their own fiscal autonomy.

The Legislature took another layer of that autonomy away this year with the passage of House Bill 1026, now Act 96. It will undercut the ability of local governments to set tax and budget policies that work in their local communities. Specifically, it prohibits local governments from levying income taxes.

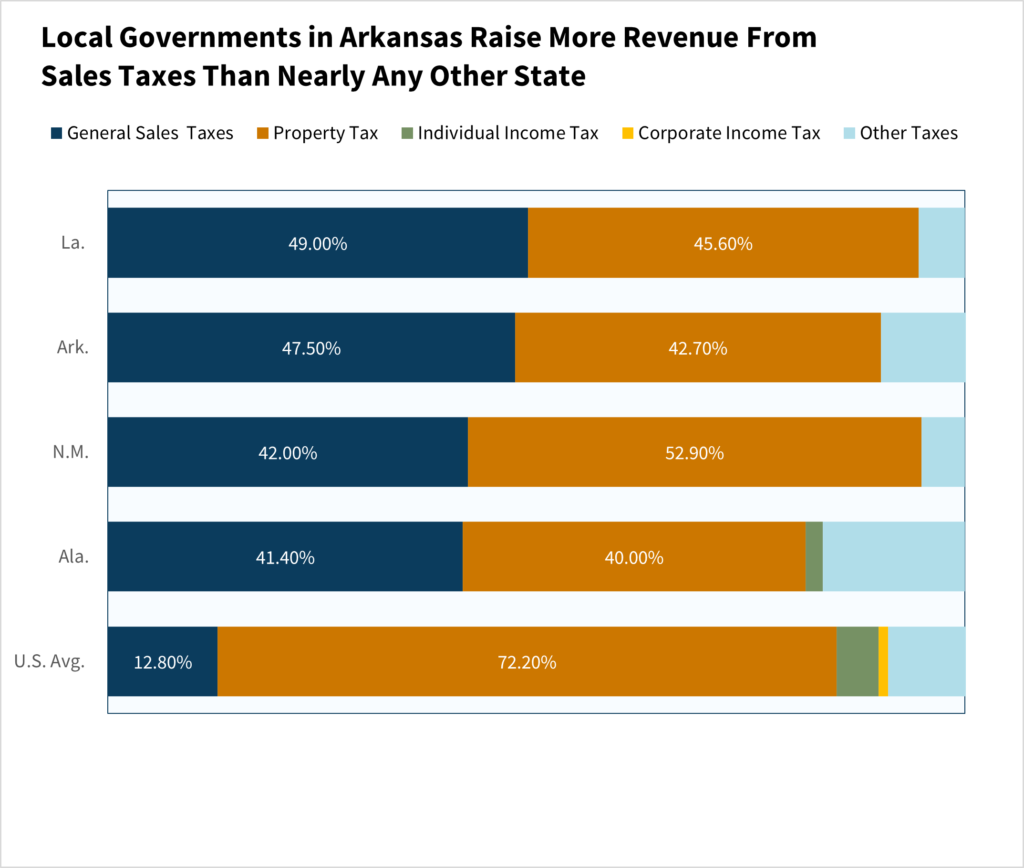

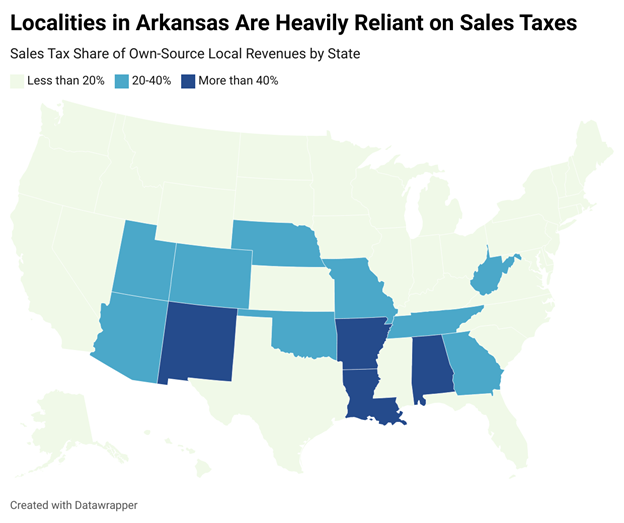

Property taxes, the primary source of local revenue in most states, are already strictly capped and managed by state mandate in Arkansas. Limiting local fiscal autonomy further by removing their ability to levy income taxes will make our localities more reliant on sales and excise taxes than they already are – and they are already far more reliant on those regressive taxes than most states.

Local governments raise more than 20% of their own-source revenue from sales taxes in only 13 states. That number falls to just four for local governments that raise more than 40% of their own-source revenue from sales taxes.

But an overreliance on sales taxes comes with several attendant issues. For one thing, the sales tax base is shrinking over time as a share of our economy as we continue to shift employment toward services and away from the production of material goods. Most services, unless specifically enumerated, are not subject to sales taxes in the way tangible goods are.

This shrinkage also has big implications for fiscal disparities between local governments. Larger cities with higher concentrations of retailers can raise more revenue than rural jurisdictions with less commercial activity. Since residents of smaller communities often – and sometimes by necessity – shop in larger and denser cities, in some sense the reliance on local sales taxes shifts revenue toward political jurisdictions in metropolitan areas and away from rural communities.

Local income and payroll taxes face some of the same issues in terms of fiscal disparity, but they have some significant upsides as well.

But whether a local income tax is a good choice for a community should be a decision that arises from that community itself. And, as the Legislature seeks to reduce and eliminate our state’s personal income tax, it will be especially important for localities to be able to retain a diverse source of revenue.