Investing in all families grows the Arkansas economy.

Many Arkansas families struggle to meet basic expenses, such as housing, food, transportation, medicine, and child care costs. The goal is for income to exceed these expenses, and parents work hard to make this happen. When it does, do those parents give away the “extra” income? Of course not. Instead, they invest in the family. This may involve opening a savings account to create a “rainy day” fund. It may be setting aside the extra income, and adding to it over time, to buy a new car, to place a down payment on a new home, or to build a college fund. Thus, parents invest in their families.

The state of Arkansas should do the same: invest in families. When income from taxes and other sources exceeds the budget, the state has a surplus. Which has often been the case in Arkansas over the past decade. What can the state do with a surplus? It can invest in programs to make housing and child care more affordable, it can enhance public education “wrap-around” services such as afterschool and summer programs, and it can improve infant and maternal health. In short, the state can invest to lift children and their families out of poverty.

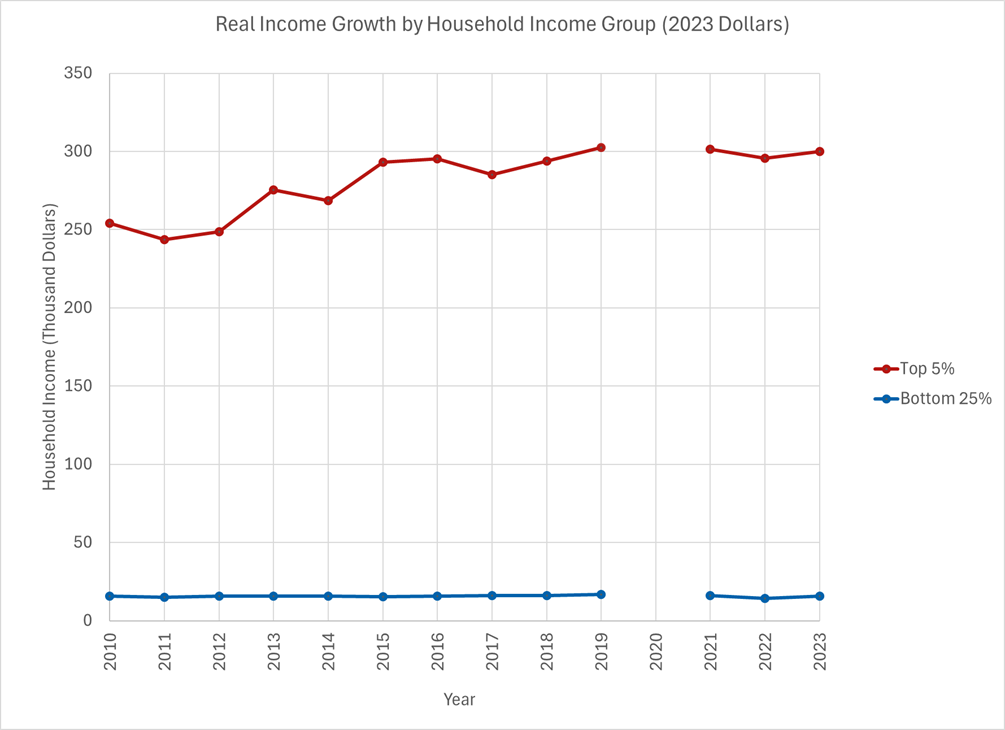

But this is not the path the state of Arkansas has chosen. Instead, the state has given away this surplus, this “extra” income. The cumulative impact of more than 10 years of income tax cuts has resulted in a reduction of more than $2 billion in general revenue annually. Think what the state could accomplish if it had this money to invest in Arkansas families every year. These tax cuts have gone mostly to the highest corporate and individual earners. Some policymakers claim that these cuts at the top help all Arkansans. But that’s just not the case, or we would see similar growth in real income at all income levels. In other words, when we control for inflation to measure “buying power,” we would see the income of low-income families grow at a similar rate as high-income families. But as the figure demonstrates, real income for the lowest 25% of households is relatively stagnant, while that for the top 5% of households is anything but:

The disproportionate effect is stark when various groupings of top-income households are compared to the low-income group:

| Household Income Group | Percent Growth in Real Income, 2010-2023 |

|---|---|

| Top 1% | 26.4% |

| Top 5% | 18.0% |

| Top 10% | 12.5% |

| Top 25% | 8.5% |

| Bottom 25% | 0.8% |

Source: AACF analysis.

Opportunity Insights measures household income at age 27 for two cohort groups: those born in 1978 (age 27 in 2005) and those born in 1992 (age 27 in 2019). For the lowest 25% of household earners, the average income is lower for the 1992 cohort than for the 1978 cohort in 37 of the 75 Arkansas counties. In other words, in just under half of our counties, 27-year-olds in 2019 were making less than their counterparts did in 2005. In fact, in eight counties, the lowest earners saw a double-digit percentage decrease in household income over this time period.

Income tax cuts primarily for wealthy corporations and individuals have not helped most Arkansans. What’s an example of a better investment? A state-level child tax credit. We know child tax credits work. According to the Center on Budget and Policy Priorities, child poverty reached a record low in 2021 thanks to the American Rescue Plan’s Child Tax Credit expansion. In fact, child poverty decreased by 46% from 2020 to 2021 (and after the expansion expired, the rise in the child poverty rate in 2022 was the largest in 50 years).

Using the state budget to invest in children and families is not only the right thing to do, but it also makes good economic sense as well. We’ve all heard the expression, “It takes money to make money.” Our policymakers should invest in all people, as economically prosperous families drive the Arkansas economy. We all thrive when we all thrive.